EVA® and Operational Analysis

5/20/2013

The objective of all corporations is to create value for shareholders. One way to achieve this is by improving a firm’s operations. Although the principle is straightforward, determining exactly what improvements should be carried out to increase or at least sustain the overall value of the firm remains a challenge for management.

Many organizations, particularly those in the manufacturing industry, have in one way or another made significant investments in initiatives such as TQM, Lean, and Six Sigma. Yet, managers still struggle with one basic question: “How does implementing these initiatives impact the value of the company?”

The next sections look at supply chain management in general and introduce a framework to answer the above question by introducing Stern Value Management’s value philosophy, Economic Value Added (EVA®). Its accompanying Value Based Operational Analysis will help management direct its efforts and investments to maximize overall firm value.

The Supply Chain from an EVA Perspective

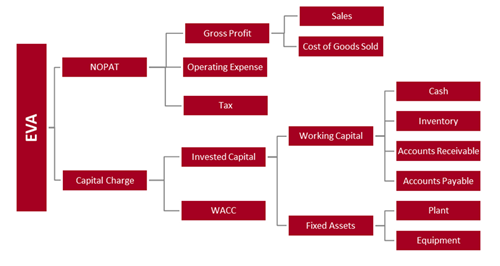

First, we need to define what value is and how it should be measured. Economic value is created only when the return on all invested capital exceeds the cost of capital. This can be best measured by EVA, which is simply Net Operating Profit After Tax (NOPAT) minus the capital charge, or the spread between a company’s rate of return and Weighted Average Cost of Capital (WACC) multiplied by the invested capital. EVA is different from other performance measures: it properly accounts for all complex trade-offs among value drivers by simultaneously capturing both operating profit and invested capital.

Supply chain management generally focuses on enhancing revenue and reducing total operating costs. From an EVA perspective, this considers only the NOPAT portion of the value driver tree shown in Figure 1, and thus represents an incomplete picture of true value creation. Maximizing operating profit this way may overlook additional capital required to support profit improvement, which consequently leads to value destruction at the firm level. For instance, a small increase in sales would not be justifiable if it came with a corresponding significant increase in capital (i.e. production capacity). Another example would be if a company were to produce to full capacity rather than to the level required to lower unit product cost: this decision could increase total cost by creating unnecessary inventory of finished goods.

Each improvement initiative is likely to affect a number of EVA drivers simultaneously. Implementing EVA will provide a common financial language for all employees in the organization – from the highest to the lowest levels – to understand and communicate the impact of their actions on others and on the whole supply chain.

Figure 1: EVA Value Driver Tree

Drilling Down Value to Operations

As elaborated in the previous section, EVA is the most comprehensive performance measure of value creation because it takes into consideration all value drivers as well as their interactions with each other. This strength of EVA enables it to be powerful at the consolidated firm level. At the division and process levels, other key performance indicators are usually used to evaluate performance. EVA may seem farfetched for division heads and process owners because they can influence only a limited number of value drivers. In other words, their ability to make a significant impact on overall EVA may appear limited or even cancelled out by other value drivers that are beyond their control.

At the operational level, EVA Contribution rather than EVA should be used to assess performance. EVA Contribution is the share that division heads and process owners can make to overall EVA. It is a partial measure of EVA that only includes the value drivers that are directly influenced by the responsible personnel. Let us use an example to further explain the difference between EVA and EVA Contribution.

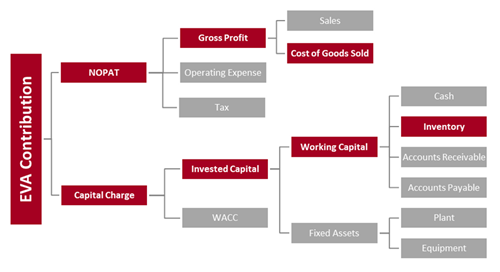

A company decides to set up a plant to manufacture beds and tables. It built the plant and bought the necessary equipment and tools for production. The EVA for this manufacturer therefore equals the NOPAT from the sale of beds and tables less the capital charge on the investment of working capital, plant, and equipment. However, as far as a production manager is concerned, he can only decide how much to produce given the existing equipment and tools on hand. That is, the production manager can only influence the cost of goods sold on the NOPAT side of the EVA value driver tree. Likewise, he can only influence inventory on the capital side. The EVA Contribution of the production manager is therefore a trade-off between the gross profit and cost of capital tied up in inventory as indicated by Figure 2 below. By continuously improving EVA Contribution, the production manager ultimately creates value for the company.

Figure 2: EVA Contribution of a Production Manager

Value Based Operational Analysis

Once the financial goal is clear, Stern Value Management’s Value Based Operational Analysis can set the stage to help companies quantify and actively manage the trade-offs among the different EVA drivers. Although value driver analysis shows the impact of a decision on EVA, it does not recommend the best action to take to maximize EVA given a set of constraints. This is where Value Based Operational Analysis comes into play.

Value Based Operational Analysis encompasses a wide variety of best practice tools customized to specific client needs. It defines, analyzes, and streamlines processes whose relationships can be modeled to help management choose sound and scientifically derived solutions and alternatives. It is a methodology that encourages extensive employee involvement, development, and participation. Because of its holistic and long-term view, regardless of where or at what level it is implemented in the organization, Value Based Operational Analysis ensures that all actions and recommendations contribute to the overarching goal of creating shareholder wealth.

Let us continue to discuss the previous example.

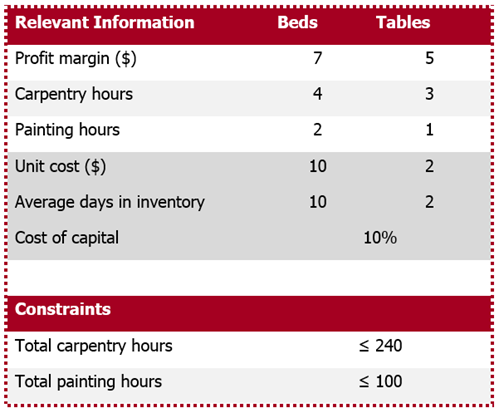

Table 1 shows the information that the production manager possesses to help him decide on a production schedule. From the conventional profit maximization perspective, it seems logical to produce more beds because they have a higher profit margin than tables. On the other hand, it is also logical to manufacture tables because more can be produced with less carpentry and painting hours than beds. However, this profit focused approach ignores another essential cost of production, the cost of working capital, i.e. the cost of inventory in this case. Value Based Operational Analysis differs from conventional operational analysis in that its goal is to maximize value rather than to simply maximize profit.

Table 1: Production Mix Example Problem

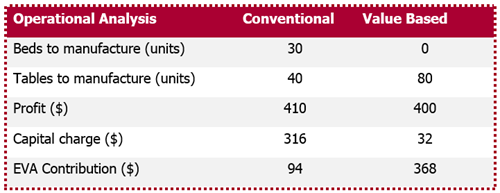

Using spreadsheet optimization, we are able to find the best production mix according to both conventional operational analysis and Value Based Operational Analysis, as shown in Table 2. Conventional operational analysis tells us that the production manager should produce 30 beds and 40 tables to generate the largest profit, $410. However, once average days in inventory and capital charge on inventory are considered, this production mix no longer brings the most value to the company. Value Based Operational Analysis instead recommends producing only tables. If the company produces only tables, the benefit of savings in capital, carpentry hours, and painting hours greatly outweighs the cost of a lower profit margin. Producing 80 tables and no beds will deliver an EVA Contribution of $368, which is much higher than the $94 that are generated when 30 beds and 40 tables are produced.

Table 2: Production Mix Example Solution

The capital charge is an important EVA driver that is often neglected in traditional supply chain management theories. Disregard of the capital charge could lead to overinvestment on seemingly profitable but actually value destroying initiatives, or underinvestment on seemingly less profitable but actually more value creating initiatives.

Stern Value Management’s Value Based Operational Analysis and its accompanying metrics, EVA and EVA Contribution, are robust and comprehensive and can be applied to measure the performance of the entire supply chain. This value framework helps all levels of management make correct decisions and quantify the impact of their actions that will, in the end, create value for the firm.