Capital Structure—Debt in Times of Uncertainty

8/21/2020

Capital structure is a crucial topic in corporate finance. All companies, regardless of industry, must confront the same issue: how much capital should be financed from debt and how much from equity? While debt may be considered by some as being “cheaper” than equity, in times of uncertainty, high levels of debt can significantly increase the risk of insolvency.

Just in February this year, the US unemployment rate was at a fifty-year low of 3.5 percent, and on February 19, the S&P 500 Index set a record high at 3,386. And then COVID hit. While the S&P has recovered most of the recent losses and is close to a record high, an unemployment rate below 4 percent seems like a distant dream. Other macroeconomic indicators like GDP and consumer sentiment have seen historical or multi-decade lows. In addition, the most recent recovery in the market is mainly driven by tech firms. Apple, Microsoft, Amazon, and Facebook now account for over 20 percent of the S&P 500 value, and all have recently hit all-time highs.

The reality for most other firms is markedly different than it is for the tech heavyweights. Epiq AACER reported 3,604 new commercial Chapter 11 bankruptcy filings for the first half of 2020, compared with 2,855 for the same period last year. It includes some household names like Hertz, J.C. Penney, and Chuck E. Cheese.

In our quest to understand how the recent uncertainty impacts business, we have closely followed S&P 500 companies. One of the questions we looked to answer is whether capital structure has an impact on a firm’s share performance. While there are many uncertainties associated with the prevailing crisis, one thing is clear from our research: bankruptcy risk is increasing every day, and hence, debt repayment capacity is weighing more on a company’s performance.

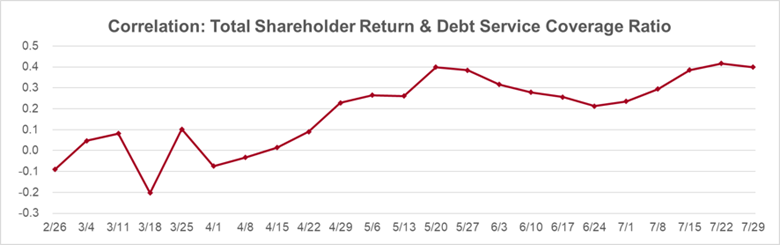

Graph 1 (below) displays the trend in the correlation between Total Shareholder Return (TSR) and Debt Service Coverage Ratio (DSCR). Total Shareholder Return is calculated as the average return for the industry from February 19, 2020. It measures how various industries have performed during this economic slowdown caused by coronavirus. Debt Service Coverage Ratio is calculated as operating income divided by current debt obligation, which includes both short-term debt and interest expense. This ratio measures an industry’s ability to generate enough income to cover its debt payments.

Graph 1: Trend in Correlation between TSR & DSCR

Back in February/March 2020, when investors shrugged off the impact of the virus or saw it as a temporary nuisance, the correlation between Total Shareholder Return and Debt Service Coverage Ratio fluctuated around 0, indicating Debt Service Coverage was unrelated to the movements in the stock prices for the period. However, as lockdowns around the world started impacting supply chains and operating incomes reflected the decrease in demand for several products and services, exhausted cash cushions made it harder to pay down principals and interest due. Thus, the correlation between Total Shareholder Return and Debt Service Coverage Ratio started trending upward. By the end of July, it had climbed to 0.4. If the situation continues to deteriorate, bankruptcy will become a more imminent threat and the correlation will likely rise further.

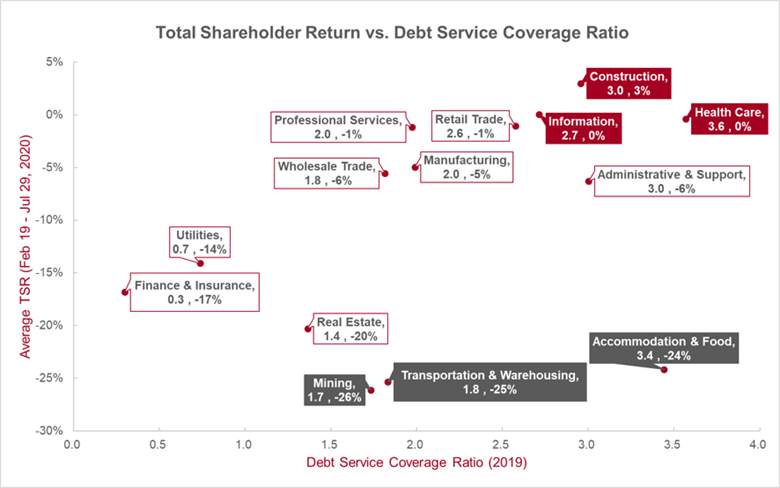

We further explored this relationship by looking at TSR vs. DSCR, by industry, to understand those whose returns were more susceptible to changes in their ability to pay their debt.

The top three performers are Construction, Information, and Health Care with marginally positive returns. These three industries also have relatively high Debt Service Coverage. The bottom three performers are Mining, Transportation & Warehousing, and Accommodation & Food, all of which have lost more than 20 percent in market value.

The Debt Service Coverages for Mining and Transportation & Warehousing are in the lower end of the spectrum, thus these two industries are more vulnerable when economic slowdown occurs. The only exception is the Accommodation & Food industry, whose Debt Service Coverage is among the highest of the fourteen industries. However, hotels and restaurants are hit the hardest by the travel restrictions and lockdowns in place. Adverse macro factors significantly outweigh the industry’s debt repayment ability in determining its stock performances.

Graph 2: TSR vs. DSCR by Industry

Conclusion

When deciding on how much debt to raise, a company should balance the low cost of borrowing and the potential bankruptcy risk caused by default in debt obligations. Finance executives need to determine the optimal capital structure for their business, the debt and equity mix, where cost of capital is at the lowest level it could be without any adversarial impact on the continuity of the business.

After money is borrowed, a company should keep monitoring the payment schedules and reviewing its debt service capabilities. It is advisable to run stress tests from time to time and come up with some backup plans to prepare the business for the unexpected.

No one can predict the future. But firms can still take measures to place themselves in better positions during challenging times.