Indonesia in Southeast Asia: Moving Up the Value Chain

8/18/2014

As Stern Value Management has done annually, this year we have looked at the wealth creation of the 100 largest Indonesian and 100 largest ASEAN (Association of Southeast Asian Nations) firms over the last 5 years. In order to measure wealth created by firms, we use the Wealth Added Index (WAI™), a methodology developed by Stern Stewart to measure firms’ wealth creation for shareholders over a specific period of time. The creation of shareholder wealth is defined as the generation of Total Shareholder Returns (TSR) above the minimum return expected by shareholders, also known as the cost of equity.

For the first time since this annual ranking started, four Indonesian firms rank in the top five wealth creators in the ASEAN. Our ranking correlates almost perfectly with Indonesia’s trek up the development ladder; over the last 5 years, the Indonesian economy has expanded the most among all ASEAN economies. Furthermore, the government has effectively reduced the cost of capital of Indonesian firms and consequently made a positive impact on the wealth creation of local firms. Yet our ranking shows the importance of not just macroeconomic growth, but also sound management practices and financial policies.

Over the last five years, Indonesia’s GDP has grown 72% in dollar terms, from US$ 510 billion in 2008 to US$ 878 billion in 2012. Furthermore, the average Indonesian has become wealthier: GDP per capita has increased 64%, from US$ 2,172 in 2008 to US$ 3,562 in 2012. This increase reflects the significant expansion of the Indonesian middle class: this new middle class, which only a few years ago looked to cover basic needs, is now purchasing more higher-end goods than in previous years. Previously content to take public transportation, the Indonesian middle class is now looking to buy its own cars and motorbicycles. Previously without bank accounts or credit cards, the middle class Indonesian now has several accounts and owns credit cards in order to benefit from better dining and services. Previously a buyer of only basic food items at the local market, he or she now buys packaged brands in super and hypermarkets. Hence, it is not surprising to find that the top five Indonesian companies in our ranking have benefitted from the expanding middle class.

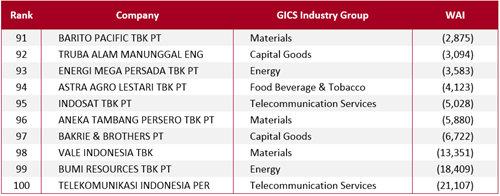

On the other hand, the bottom of our Indonesian ranking highlights the poor performance of commodities firms. Indonesia’s main export is commodities; because of the fall in Indonesia’s exports from 30% of GDP in 2008 to 24% of GDP in 2012, we are not surprised that commodities firms’ performance has been abysmal. This is due to various reasons. First, government intervention and excessive regulation continue to be a drag on mining firms. Second, the collapse of coal prices from US$ 125.31 per metric ton in late 2011 to US$ 93.64 per metric ton at the end of 2012 has hurt firms’ performance. Third, as our study shows, poor corporate governance, a lack of adequate management systems, and excessive debt were equally detrimental to performance.

Table 1. Indonesia - Top 10 Wealth Added Index (WAI) Ranking

* Figures expressed in millions

USD Source: Bloomberg

Note: GICS is the Global Industry Classification Standard and is the registered trademark of Standard & Poor’s and MSCI

Table 2. Indonesia - Bottom 10 Wealth Added Index (WAI) Ranking

* Figures expressed in millions USD

Source: Bloomberg

A governance study on Indonesian firms shows that the country is trailing most of its regional peers. Governance at Indonesian firms must change if they would like to continue leading regional performance rankings. From the end of 2012 to the end of the first quarter of 2013, other regional indices have performed well. During this period, Singapore’s STI index has grown by 4.5%, Thailand’s SET Index has grown by 12.2%, and the Philippines’ PSEi Index has grown by 17.8%. So while the Indonesian IDX has performed very well, growing by 12.5% in the same period, Indonesian stock performance is likely to be challenged by the end of 2013. Furthermore, while the Indonesian government seems keen to chase away foreign firms from investing in the country (think of regulations in mining and oil and gas), it has started to realize that foreign firms will create local jobs and push local firms to be more efficient. As a result, the government has stopped interfering in some industries. Among positive indicators is Coca Cola’s announcement early this year that it plans to spend US$ 700 million in capital and marketing expenditures over the next 3 years in Indonesia, citing the growth of the country’s middle class. This exemplifies that going forward, local firms will be tested by global competitors more than ever.

Table 3. Asean - Top 10 Wealth Added Index (WAI) Ranking

* Figures expressed in millions USD

Source: Bloomberg

Excessive debt is also a problem. Investors generally avoid firms from which banks are likely to demand large interest payments. This is supported by the fact that, as of the end of 2012, the top 10 performers (excluding banks and insurance companies) had an average debt to equity ratio of less than 50% while the worst performers (excluding the aforementioned companies) had an average ratio of about 90%. Likewise, during my years of experience in the region, I have frequently run into firms that use short-term debt to finance long-term projects: nine out of ten of these companies eventually run into severe debt problems that cause investors to look for other pastures.

Table 4. Asean - Bottom 10 Wealth Added Index (WAI) Ranking

* Figures expressed in millions USD

Source: Bloomberg

The previous example is a signal that internal governance systems are lacking. This is usually caused by a misalignment of incentives. Most investors look for firms that will provide long-term returns, yet most internal governance systems encourage short-term profitability. Think of the number of firms that look at EBITDA as a measure of performance; unfortunately, EBITDA completely ignores the costs of long-term investments and the interest charged to finance them. Proper governance systems look to align shareholders and management and move firms a step closer to ensuring proper returns to shareholders.

Indonesian firms have benefited from the significant growth of the country’s middle class and government policies that have reduced the cost of capital. While these two conditions are unlikely to change in the next few years, the upcoming election, the expansion of other regional economies, and the investments made by foreign companies in the country are likely to affect the hegemony of Indonesian firms at the top of Stern Stewart’s 2014 ranking.