Minimize the Value Destruction: Management's Commitment in Time of Crisis

7/30/2020

In the face of this unprecedented global economic crisis, companies have been forced to make quick decisions in order to survive. Many of them have focused on taking care of their cash flow. Nonetheless, the desperate search for liquidity should not displace the main corporate objective of maximizing long-term shareholder value.

While advising clients on issues related to Capital Allocation (M&A, investment in projects and divestments), we insist on keeping in mind the firm’s strategy. Before approving a new investment, before suspending projects or divesting assets, the impact that these actions may have on the company’s strategy must be thoroughly analyzed. For this, it is important to look into the following factors:

Direct effect on the company’s operations:

- Does the decision jeopardize current operations in any way?

- Is the decision essential for an expansion project?

- Does the decision help ensure the sustainability of the current business?

Impact on strategic factors:

- Does the decision jeopardize the relationship with suppliers, government, customers, or any key stakeholder?

- Does the decision affect any strategic partner?

This analysis of each opportunity allows us to understand the importance of each project or asset to the firm’s strategy. If the alternatives are not aligned with the firm’s strategy, they will need to be re-evaluated and new options should be explored.

There is also a need to ensure that cash, risk, and value creation are aligned. It becomes extremely important to prepare a weekly cash flow projection where all line items/inputs are optimized. Costs and expenses must be re-evaluated, working capital optimized, and debt renegotiated.

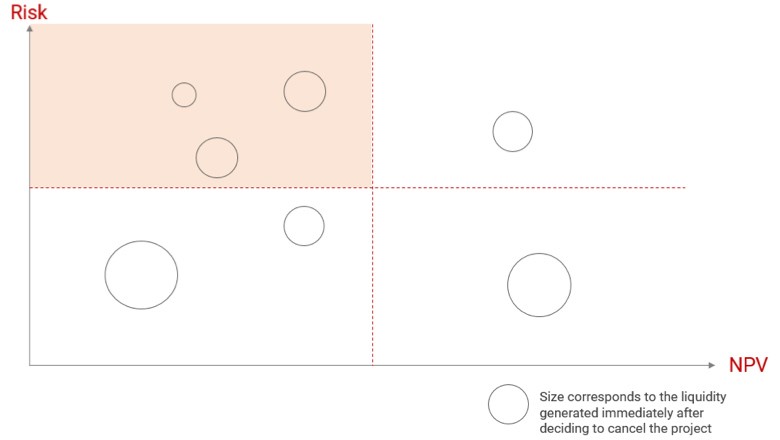

Once a strategic analysis of each asset and project has been made and sources of cash have been identified, a good practice is to make a value creation vs. risk matrix. This matrix considers various risk elements, including the volatility of the projected cash flows. This will help us benchmark projects not only on their ability to create a positive Net Present Value (NPV), but also on the volatility and uncertainty of its value creation potential. This will allow us to identify which projects may be more suited to suspend or cancel in times of uncertainty.

Graph 1

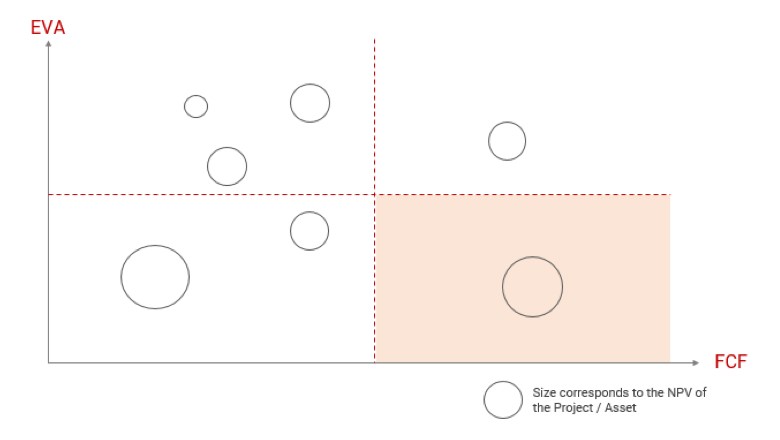

When it comes to ongoing projects, an EVA® (Economic Value Added) vs. Free Cash Flow analysis is important. This analysis will allow us to identify those projects that create value but are not generating cash flow in the short term and those that generate cash flow but are not accretive to long-term value creation. This will enable management to make decisions that help alleviate cash flow issues in the short term, while minimizing the potential destruction of value.

Graph 2

To summarize, the first step is to keep the corporate strategy front and center. Subsequently, projects that have yet to generate cash flows should be put through an NPV vs. Risk analysis which provides a filter to identify project candidates that should not be pursued. Finally, ongoing projects should be put through an EVA vs. Free Cash Flow analysis to determine which should be suspended or cancelled to conserve cash flow while keeping the ability to maximize long-term shareholder value intact.

Although the recent uncertainty has shown the importance of cash flows to ensure the survival of organizations, attention cannot be diverted from the importance of measuring value creation. Not all projects or assets that generate greater profitability or higher income create the most value. This is why EVA must reign supreme over other metrics as it takes into account the invested capital, the operating profit of the company, and the opportunity cost for shareholders.