Now is the Time to Re-examine Your Capital Structure

Now is the Time to Re-examine Your Capital Structure

5/3/2021

Today’s rapidly evolving and volatile macroeconomic environment requires corporate executives to evaluate whether their current capital structures are optimized for ongoing shareholder value creation.

Macroeconomic environment

Historically low interest rates (though they are rising fast), expected inflation, projected global economic recoveries following pandemic lockdowns, and fiscal stimulus are major driving forces in today’s (and tomorrow’s) economic outlook. These macroeconomic factors affect capital structure decisions through their impact on firm value and the cost of capital.

What is capital structure?

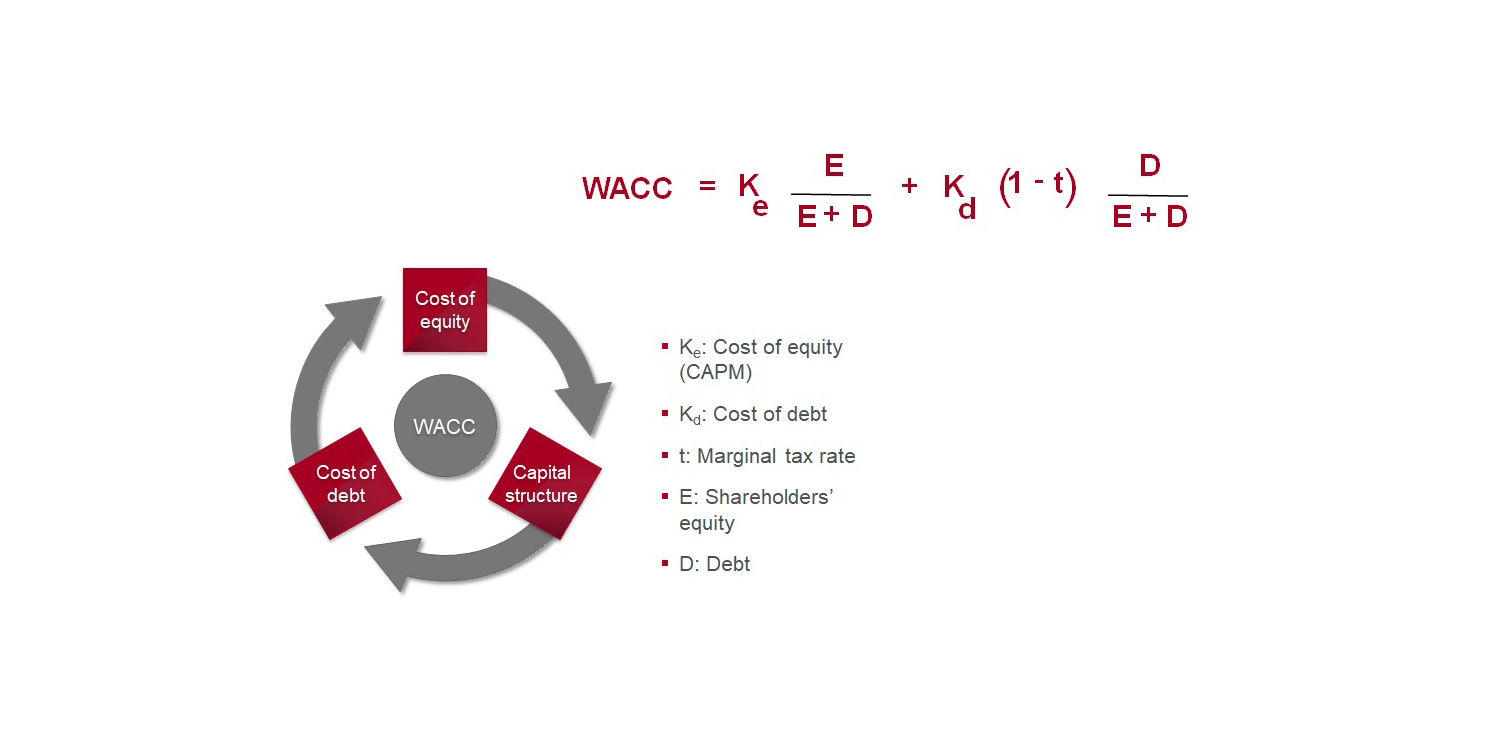

Capital structure is the allocation and/or weighting for each instrument in the portfolio of items on the righthand side of the balance sheet. Critical to understanding whether one’s capital structure is optimized is understanding the weighted average cost of capital (WACC) and how it impacts capital structure.

Understanding the critical role of the cost of capital

Increasing or decreasing leverage has a direct impact on a company’s credit ratings. These credit ratings weigh heavily in determining at what cost the company can take on new debt, a metric known as cost of debt.

The cost of debt is intricately tied to the risk that investors take on by acquiring more equity in the company, thus affecting the other half of the equation, i.e., the cost of equity (reflected by the beta).

In today’s environment, both sides of the equation face new opportunities and challenges. Historically low interest rates can lower the cost of debt for companies (depending on credit rating, capital market liquidity, among other factors). Meanwhile, asset inflation can result in the movement of more investor funds into the market, thereby facilitating equity financing and/or trading volume. Further, volatility versus the market index affects beta and the most distinguishing feature of today’s market activity continues to be volatility.

Key considerations when considering an optimal capital structure

Instruments

Today's markets provide a plethora of financing options, from more rigid and traditional to new and creative. The following need to be taken into account when considering various instruments for rebalancing capital structure:

- How much flexibility does this instrument provide us?

- Is it appropriate given our circumstances to use the equity lever (e.g. buybacks) in order to shift structure?

- Can we incorporate mezzanine capital into the mix instead of thinking in purely binary debt/equity terms?

- What benefit does the instrument provide to investors?

- Is this instrument a derivative and what role do exogenous forces play in the underlying instrument?

Risk Management

Effective risk management requires humility, recognizing that we cannot predict the future and most forecasts are inaccurate during the times we need them most, i.e., times of disruption and high volatility. Most times we do not think of capital structure through a risk-managed lens, but by doing so, we can create more antifragile (i.e., not only resilient to volatility, but benefitting from it) capital structures and respond to a wide host of unforeseen circumstances.

Ask yourself the following questions when considering the risk management aspects of capital structure optimization:

- How much flexibility does my current and target structure offer me (flexibility is critical)

- How can I profit from times of uncertainty, or at worst, hold out long enough until the environment stabilizes?

- Have I put my current and target capital structures under stress tests using varied assumptions?

- Which instruments can balance short-term and long-term capital needs, while providing maximal benefits to operations and investors?

Shareholder Value Creation

At the end of the day, investors care about one main thing: will the use of new capital create returns above the cost of that capital. If the answer is yes, then value has been created; conversely, if returns are below the cost of capital, value has been destroyed. Ignoring shareholder value creation when looking for an optimal capital structure can be perilous.

In other words, investors are primarily concerned that whichever instruments are used to raise new capital will be used on value creating projects. By keeping this value creating proposition as the North Star during capital structure optimization, companies free themselves to think more creatively and broadly about appropriate tools to shift structure. The following should be considered to ensure that this is done:

- How are we evaluating projects and capital expenditures? Are we using true value creating metrics?

- Is capital used to embark on M&A? If so, are the acquisitions really shareholder value accretive?

- How would improved economic profit impact our firm's value?

- Would the costs of a credit rating upgrade be worth the benefit?

Given the unique opportunities available in today’s markets and the quickly changing landscape, now is the time for firms to evaluate how they can achieve an optimal capital structure and provide long-term, sustainable value creation to investors.