VBM - Value Based Management™ and Economic Value Added (EVA®)

6/23/2020

Sustainable Shareholder Value and VBM

You have a business, and one day during a discussion on which strategy to pursue, one of your advisors comes in and says, “Look, this really comes down to what is our most important goal?”

How would you answer that question? What is the central goal of your business? The answer should be to create sustainable value for the owners of the company. VBM - Value Based Management™ provides a framework to achieve that goal.

VBM, once implemented, touches all aspects of business operations: from performance measurement to corporate governance to strategy and financial planning to capital allocation and incentive compensation. Here are three main ideas that are at the core of VBM:

- Long-term shareholder value creation is more important than unsustainable short-term growth.

- Economic reality is more important for value creation than accounting numbers.

- Incentives matter. Variable compensation should transform employees into partners in the creation of value.

The first step in VBM is finding the right metric(s)—the one(s) that correctly measures how much value is created. For us that quest started over fifty years ago.

In Search of the Right Metric

In the late 1960s, while working as an advisor to David Rockefeller who was chairman and CEO of Chase Manhattan Bank, our late founder and CEO Joel Stern realized that accounting and accounting-based metrics, while very useful in some aspects of running a business, did not shed light on a company’s true operating performance.

In his search for the right metric, Stern came up with Free Cash Flow (FCF), which measures how much cash is left over after all of the company’s cash transactions are recorded. The idea was born out of a conversation Stern had with an uncle who ran a convenience store. Stern had asked his uncle how he could tell when the store was doing well and when it was not. The uncle pointed to a cigar box where he held the cash and said, “Cash goes in and cash goes out of the box. If the lid is rising up, I am doing well. If not, then I’m not.” In other words, cash is what matters.

When Stern and his partners left the bank and formed what is now called Stern Value Management, FCF was the main metric used for advising corporations on how to assess performance and make value-creating strategic decisions. But the issue was that the metric had no memory. In other words, funds that were invested in previous periods no longer appeared on a FCF calculation, making it hard to judge whether an investment yielded good results and even harder to hold management accountable for making the decision to invest.

In came EVA.

EVA—The Metric at the Center of It All

Economic Value Added (EVA) improved on FCF by accumulating investments, recording them as capital, and charging a rental fee for the use of this capital. This rental charge was then subtracted from a firm’s net operating profits after taxes to arrive at EVA.

Hence, one can easily understand whether a company is creating or destroying value by looking at its EVA: if EVA is positive, the company is using its capital to create value; on the other hand, if EVA is negative, the company is destroying value. But even more important than EVA is the change in EVA from one period to the next. If a firm makes a large investment, it may cause EVA to be negative initially, so the goal should be EVA improvements over time. And since the change in EVA is highly correlated with long-term share price appreciation, we are better aligning our performance metric with shareholder wealth creation.

EVA was also an improvement on more traditional metrics such as EBITDA or Net Income. While EBITDA is easy to estimate, it ignores several aspects of a firm’s operations, including non-cash items such as depreciation, taxes, and most importantly, capital and its cost.

In addition, EVA can go further than traditional metrics by converting accounting statements into economic statements. Accounting standards can distort economic reality and therefore provide cover for value-destroying behavior. One-time actions or abnormal gains or losses can blur the true story of how a company is actually doing. Spending on intangibles such as R&D, training and development, or brand building are usually expensed in the year they are incurred instead of being capitalized and treated as investments. Further, accounting rules are often not customized to the industry in which a business operates, and therefore they can generalize data, making it more difficult to see underlying risk, value creation, and financial health of corporations. EVA can address this problem by making appropriate and personalized adjustments to accounting data in order to capture the underlying economic reality of businesses.

So What is VBM and Why Should Firms Adopt it?

After creating EVA, Stern noticed that it was not enough to just measure value creation. Value creation should be embedded in all key corporate processes for a company to have superlative performance. This led to the creation of the EVA System, now better known as VBM.

VBM is a management framework that looks to align the key corporate processes with the goal of creating sustainable shareholder value. The VBM framework covers performance management, capital allocation, strategic planning, and incentive compensation. The system, when implemented properly, answers the following questions:

- What parts of a company have contributed more to value creation?

- To which parts of the company/project should I allocate capital?

- What targets, if achieved, should justify the current valuation of the firm?

- How can we align the interests of employees and those of shareholders through a variable compensation system that shares the value employees have created?

The system’s main strength, as can be inferred from the questions it answers, is that it provides alignment between shareholders and employees, leading to a virtuous cycle of value creation for both: higher returns to shareholders, more capital allocated to the firm, more investments in value enhancing projects, and higher variable pay for employees. Win-win.

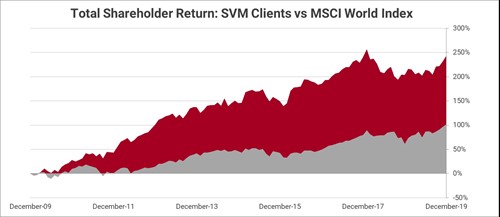

Last, but not least, companies need to adopt VBM because it works, as is clear from the following graph that displays the results of those who adopted VBM versus the most relevant benchmark.

What is your firm waiting for?